Create and Simulate¶

The definition of an ARMA model is:

where  is the lag operator,

is the lag operator,  a

a  -dimensional

vector of observed output variables,

-dimensional

vector of observed output variables,  a -dimensional vector

of white noise and

a -dimensional vector

of white noise and  a

a  -dimensional vector of input variables.

Since

-dimensional vector of input variables.

Since  and

and  are matrices in the lag shift operator, we have

are matrices in the lag shift operator, we have

is a

is a  tensor to define auto-regression,

tensor to define auto-regression,

is a

is a  tensor to moving-average and

tensor to moving-average and

is a

is a  tensor to account for the input

variables.

tensor to account for the input

variables.

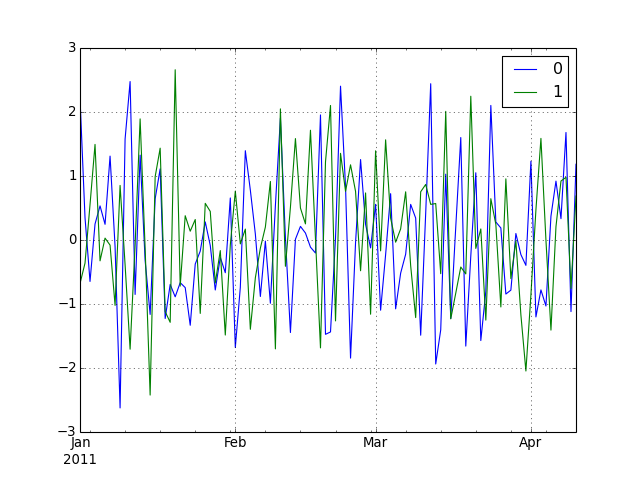

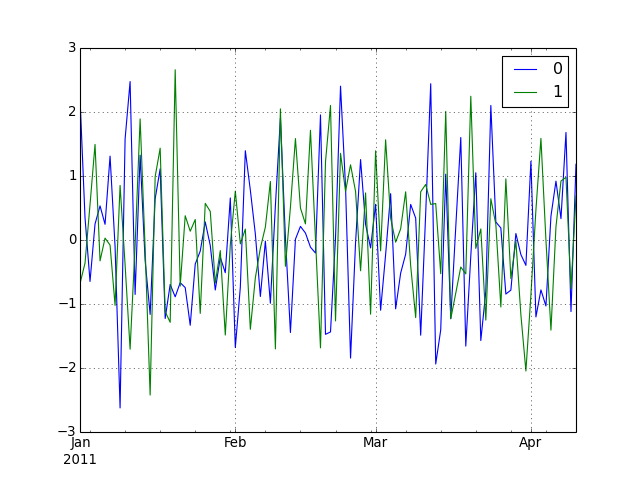

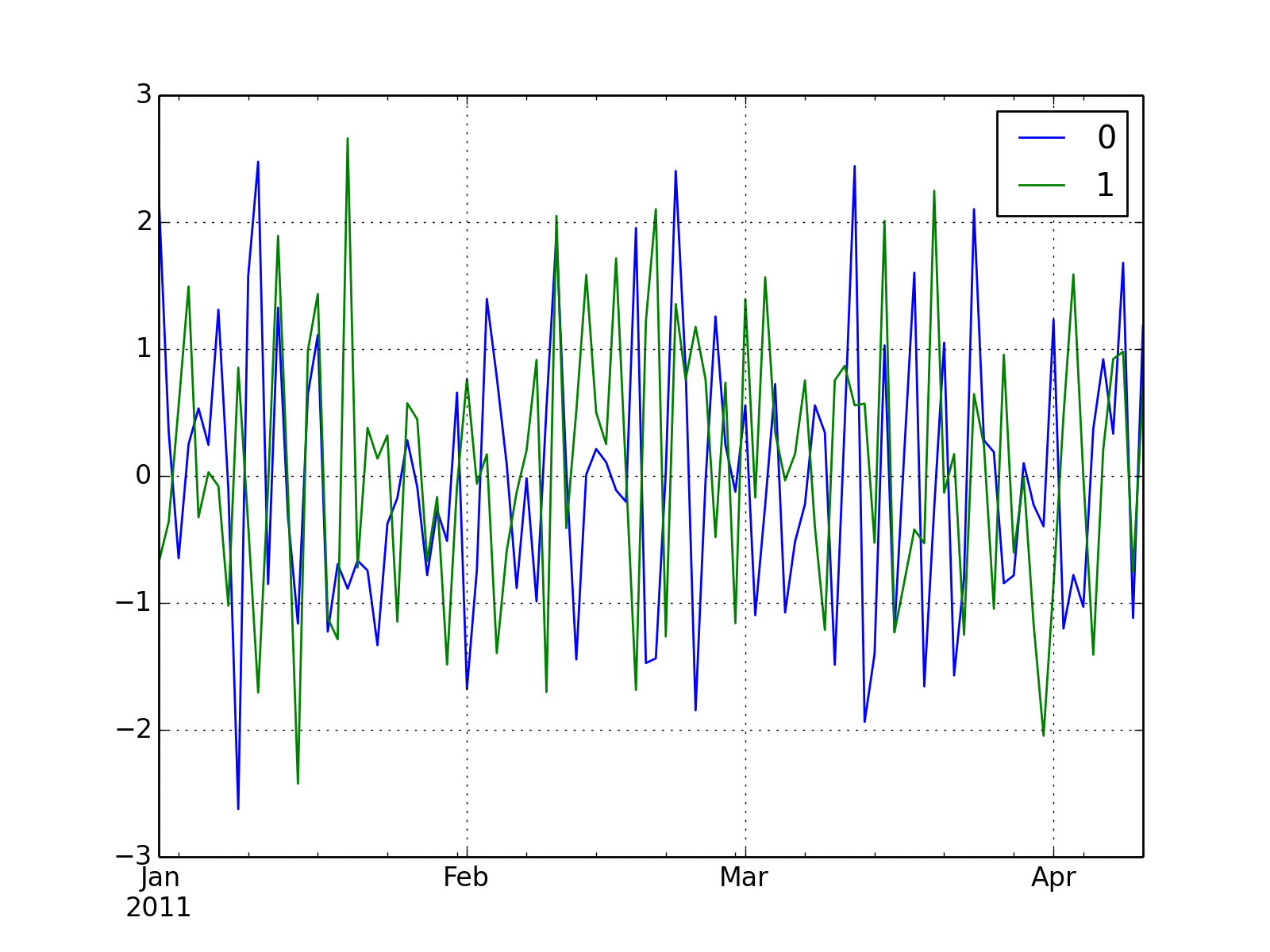

We create a simple ARMA model for a two dimensional output vector with matrices:

In order to set this matrix we just write the entries left to right, up to down into an array and define the shape of this array in a second array:

import pandas as pd

import numpy as np

import matplotlib.pylab as plt

from pydse.arma import ARMA

AR = (np.array([1, .5, .3, 0, .2, .1, 0, .2, .05, 1, .5, .3]), np.array([3, 2, 2]))

MA = (np.array([1, .2, 0, .1, 0, 0, 1, .3]), np.array([2, 2, 2]))

arma = ARMA(A=AR, B=MA, rand_state=0)

Note that we set the random state to seed 0 to get the same results. Then by simulating we get:

sim_data = arma.simulate(sampleT=100)

sim_index = pd.date_range('1/1/2011', periods=sim_data.shape[0], freq='d')

df = pd.DataFrame(data=sim_data, index=sim_index)

df.plot()

(Source code, png, hires.png, pdf)

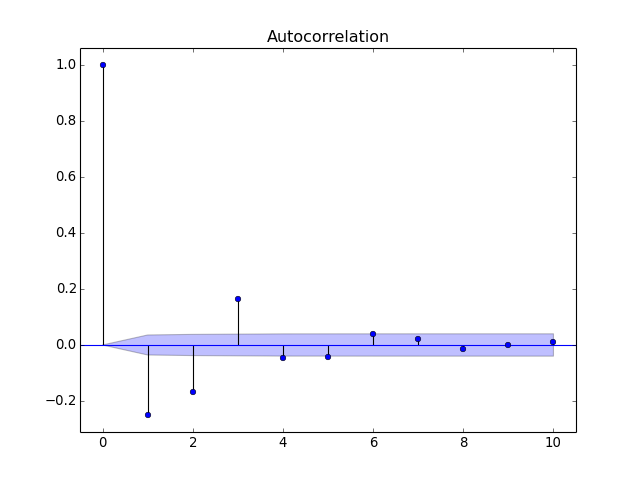

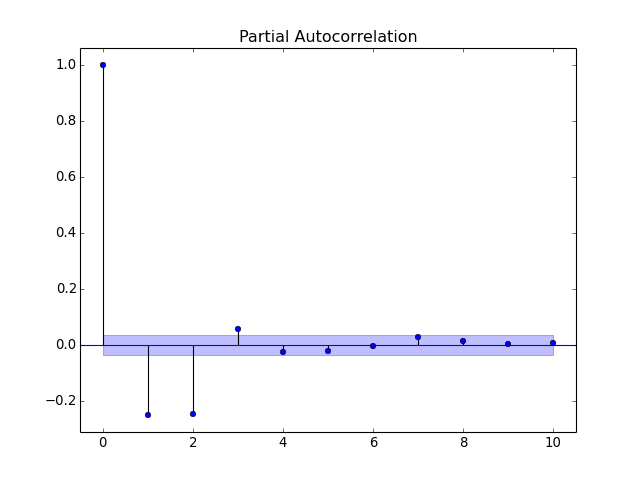

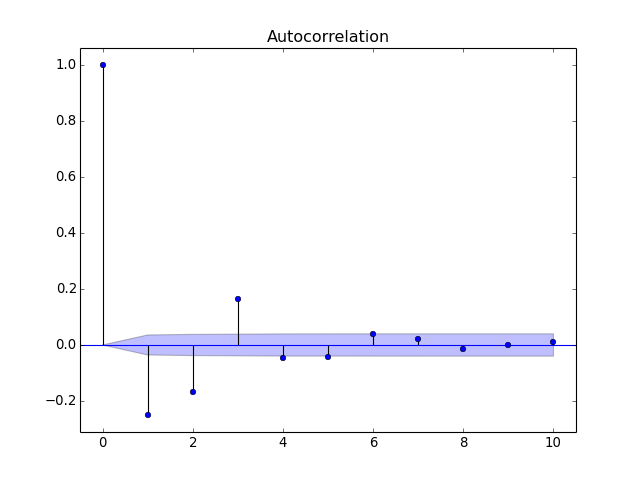

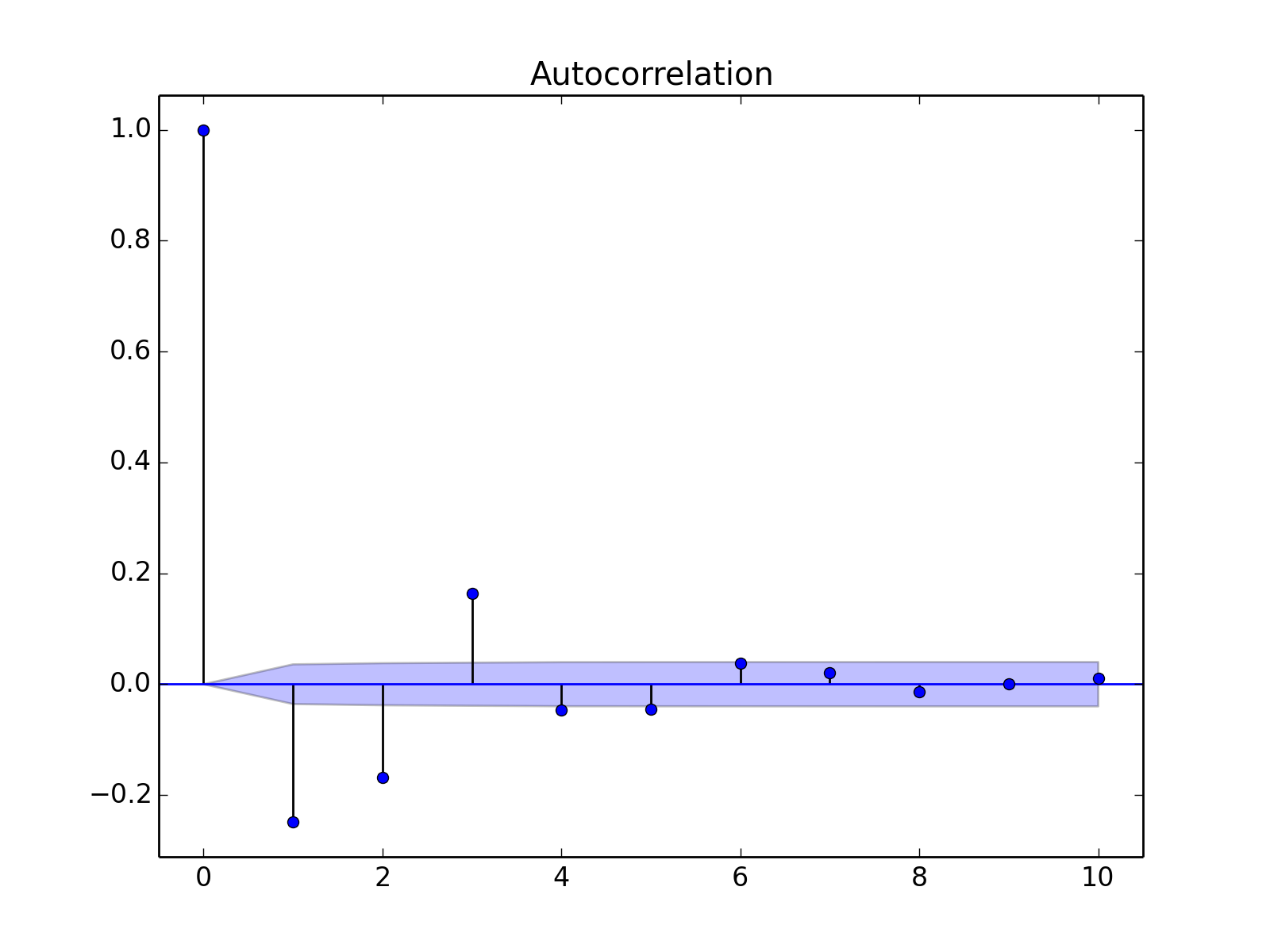

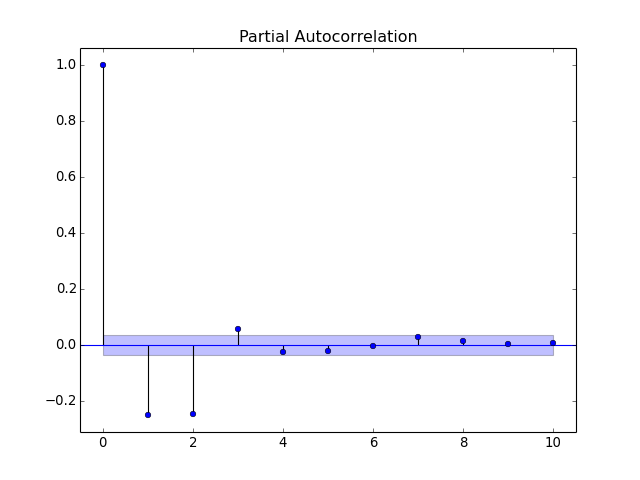

Let’s create a simpler ARMA model with scalar output variable.

AR = (np.array([1, .5, .3]), np.array([3, 1, 1]))

MA = (np.array([1, .2]), np.array([2, 1, 1]))

arma = ARMA(A=AR, B=MA, rand_state=0)

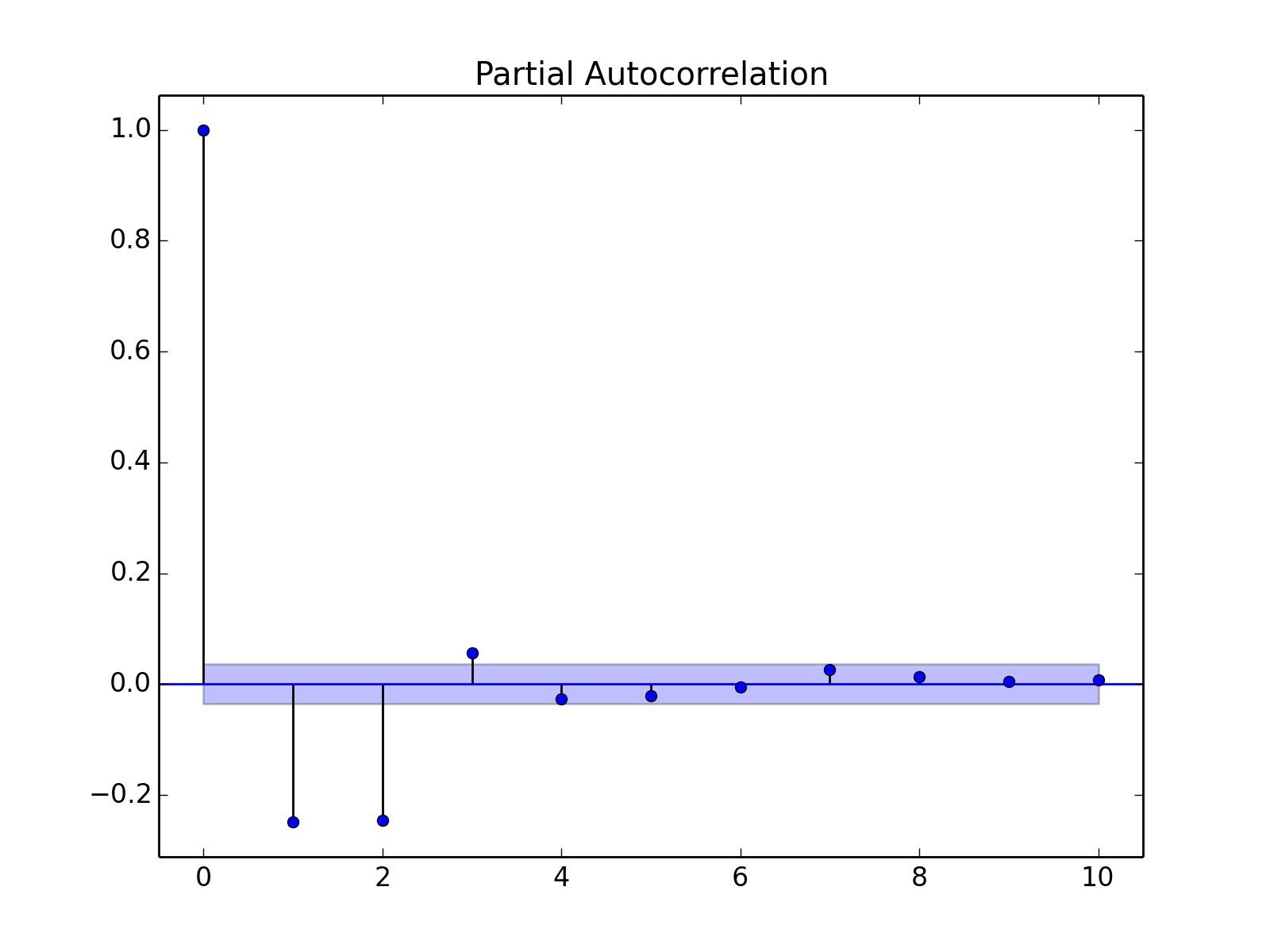

Quite often you wanna check the autocorrelation function and partial autocorrelation function:

from statsmodels.graphics.tsaplots import plot_pacf, plot_acf

sim_data = arma.simulate(sampleT=3000)

sim_index = pd.date_range('1/1/2011', periods=sim_data.shape[0], freq='d')

df = pd.DataFrame(data=sim_data, index=sim_index)

plot_acf(df[0], lags=10)

plot_pacf(df[0], lags=10)

plt.show()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Find a good introduction to ARMA on the Decision 411 course page.